Since 1995, the United States has seen a 65% increase in the cumulative rate of inflation; something you could buy back then for $1,000 would today cost about $1,675.

On a larger scope, let’s say a property that was for sale in 1995 had a listing price of $250,000. Today, that listing price would be at least $420,000.

This doesn’t take into consideration any appreciation the property has acquired — only the value of the dollar that has been changed due to inflation.

How can investors shield themselves (and even profit from) this inflation?

Using Inflation to Your Advantage with Turnkey Properties

Owning turnkey rental properties in Kansas City can provide a hedge against inflation, regardless of what happens to the value of the dollar in the future. For the most part, this is due to two main factors: rental income and fixed-rate mortgages.

Most of the time, when people purchase passive income real estate, they use money that belongs to other people through financing.

Most mortgage loans carry a term of 30 years. When possible, the investor should opt for a fixed-rate mortgage, not an adjustable one. This ensures that the payment will not change for the next 30 years – even as inflation increases.

A turnkey rental also makes a solid hedge against inflation because the owner can increase the rent through the years to keep up with inflation.

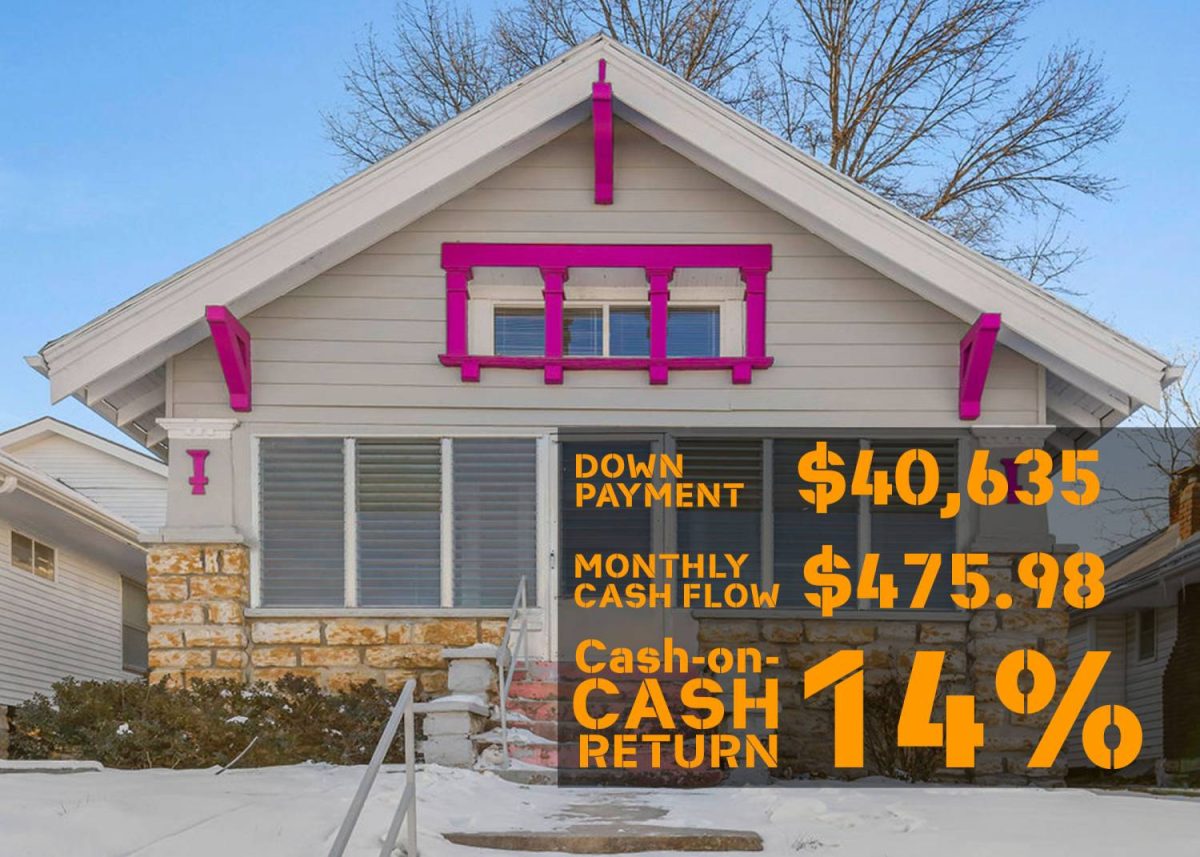

For example, an investor can charge $980 per month for rent (because other similar properties in the neighborhood have rent at about the same level), even though he or she only has a monthly mortgage payment of $720 per month.

The investor banks a nice little profit each month, and through the years, as inflation increases, that $980 per month can increase because “inflation requires it.”

The Dilemma of Traditional Investments in an Inflationary Environment

When relying solely on traditional investments like savings accounts and IRAs for retirement, individuals may find themselves inadequately prepared due to inflation. Consider a person earning an annual salary of $100,000 today, saving for retirement based on their current lifestyle and expenses. Given the pace of inflation, they would need more than double this amount in the future to maintain the same standard of living during retirement. Unfortunately, the purchasing power of the U.S. dollar does not increase proportionally with inflation, leading to a decrease in the real value of saved money.

For example, a savings account holding $50,000 today will effectively be worth only about $25,000 in 30 years if the inflation rate continues at its current trajectory. This stark decrease highlights the significant impact inflation can have on traditional savings methods. The challenge is exacerbated when you consider that the interest rates on these accounts often fail to keep pace with inflation, further eroding the real value of the money saved.

Real Estate as a Strategic Inflation Hedge

To counteract the effects of inflation, investors are turning to assets that naturally appreciate or hedge against inflation, such as real estate. Real estate investments, particularly in markets like Missouri, offer several advantages as inflation hedges:

- Increasing Income: Rental income is a robust inflation hedge. As prices increase, property owners can adjust rent accordingly, ensuring that income keeps pace with rising costs. Effective acquisition and management of turnkey properties allow for rental income not only to cover all operational costs, including mortgage, taxes, and insurance but also to generate substantial positive cash flow. This strategy provides an ongoing income stream that grows in line with or exceeds inflation.

- Depreciating Debt: For turnkey property investors utilizing amortized loans, the nominal value of debt diminishes over time as inflation rises. While monthly payments remain fixed, the real cost of these payments decreases, effectively making the debt cheaper over time.

- Appreciating Value: Real estate typically appreciates at a rate that outpaces inflation. For instance, a property bought for $100,000 is projected to increase in value annually by 3% to 5%, potentially reaching around $148,000 after ten years at a 4% appreciation rate. Meanwhile, with inflation at about 19% over the same period, the purchasing cost of a similar property would rise to approximately $119,000, demonstrating real growth in asset value.

Turnkey Properties: A Superior Solution for Inflation Challenges

Turnkey rental properties in areas like Kansas City offer a compelling investment opportunity that not only matches the pace of inflation but also provides the potential for asset appreciation and wealth accumulation. Even during economic downturns, such as those experienced between 2009 and 2012 when inflation averaged about 2%, these properties remained a reliable investment. Turnkey rentals provide a passive income stream, continuous appreciation, and an effective buffer against inflation, making them an excellent choice for investors seeking to protect and grow their wealth in uncertain times. Thus, in the battle against inflation, turnkey real estate stands out as a proactive and potent strategy for safeguarding financial stability.

Choosing the Right Turnkey Provider in Kansas City

When venturing into the turnkey rental property market, selecting the right provider is crucial. A good turnkey provider in Kansas City should offer:

- Transparency: Full disclosure of property history, renovation details, and tenant records.

- Local Expertise: Deep understanding of the Kansas City market, neighborhood dynamics, and economic trends.

- Quality Renovations: Commitment to high standards in property upgrades and maintenance.

- Reliable Management Services: Efficient handling of tenant relations, property maintenance, and financial management.

For information on how Kansas City turnkey rentals can help you reach financial freedom with passive income real estate, contact Real Deal Properties.

continue reading

Related Posts

College Ave, Kansas City, MO 64130

College Ave Kansas City, MO

Chestnut Ave, Kansas City, MO 64132

Chestnut Ave Kansas City, MO

E 48th Ter, Kansas City, MO

E 48th Ter Kansas City, MO

S Benton, Kansas City, MO

S Benton Kansas City, MO

Jackson Ave KCMO 64132

Jackson Ave Kansas City, MO